Download PDF version here | It was just a matter of time for Sony. The company is about to sell its PC business, in a long overdue move that is not a surprise to me. Having analyzed the company’s position over the past decade, characterized by a fast eroding market share, due to a massive drop in volumes amid intense competition from other Asian firms, I often wondered how far Sony would go to maintain such unsustainable status quo. Even as recently as June 2013, I spoke to some of its executives in Tokyo, as well as bankers and investors essentially telling them that selling hardware without keeping the customer afterwards is a losing proposition. Considering its brands and its rich contents of movies, music, plethora of devices, etc, Sony could have been a perfect platform provider. .[membersonly]Instead, the company’s culture prevented the emergence of a true closed-loop platform that Sony could have used to own its customers. Indeed, today’s business is all about customer stickiness that is so critical for business sustainability. And that’s something that most device makers are having real hard time understanding.

So it is now time for tough decisions. With Mr. Kazuo Hirai as its new top leader, unpopular decisions have to be taken, starting with the sale of a chemical products-related business and the company’s New York City’s building.

On the hardware front, there has been a de-emphasizing of PCs, and a refocus on Mobile, Imaging and Game businesses, or what the company qualifies as its “three core electronics businesses.” For Sony, Mobile means smartphones and tablets, and does not always incorporate notebooks and desktops. Instead, we see greater emphasis on Xperia smartphones and tablets, and a move away from Vaio. The company will continue to focus on TVs, a key business for a firm that is deeply entrenched in movies and contents. But it has decided to split off its TV unit into a separate subsidiary and invest more on the so-called 4K technology to bring much higher definition TVs in the market, and increase its margins.

So what does that mean in terms of recycling? First, the Vaio brand is probably dead, though it may not disappear altogether so quickly. Sony is selling it to Japan Industrial Partners (JIP), which is likely to inject fresh resources and a new vision. JIP business is all about investing in poorly performing industrial businesses and try to resuscitate them. That fits well with the Vaio brand, which despite lack of consumer interest; it still remains premium in the minds of many of them. It is still unclear how the Vaio brand will be distributed in the future, but expect more of it in emerging markets, and a lot less in mature markets. In the US, if you are a recycler who may have generated healthier margins with the Vaio brand, time to focus on something else.

In terms of TVs, expect a lot less volume. If the new spinoff will focus on the expansive 4K technology, and move away from the rest, quantities are likely to drop considerably and that will have an effect on TV recycling in the midterm.

On the recycling front, Sony U.S. has always been an active participant through its take-back programs. It has sponsored planned and ad-hoc collection initiatives involving retailers and waste companies, but it also maintained recycling activities to handle collection, refurbishing, remarketing, etc using a number of partners on the downstream.

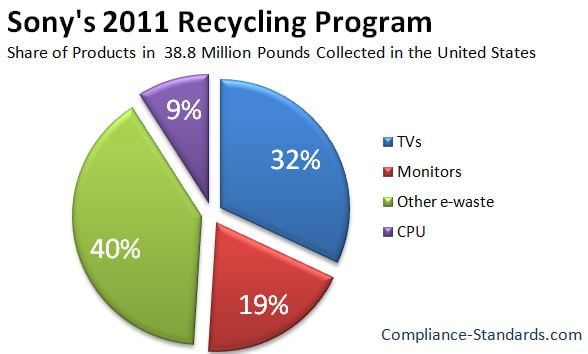

So how performing was Sony’s recycling program? To start with, the company’s US business focused greatly on TV recycling. Naturally, from a volume perspective, since the recyclers and OEMs insist on using weight as a metric, about one third of the weight it handles comes from the decommissioning of TVs. Remaining in the display space, monitors account for almost 20% of the volume, while CPUs (ie: PCs) are responsible for less than 10% of its e-waste. The remaining 40% is a collection of all of its other devices. In Sony’s recycling world, specific to the US market, displays, the sum of TVs and monitors, accounted for a great deal of collected weight. Moving away from heavy displays, monitors and PCs will mean a substantial reduction of cost related to eWaste collection.

The reports on recycling and collection programs published by most OEMs are somewhat difficult to assess. Details and audit trails are not available and therefore one has to be careful in analyzing the data.

In the case of Sony, our best assessment is that its 2011 recycling programs collected 38.8 million pounds of electronics. Most of the volume or just over 30 million pounds originated from indirect customer channels, essentially retailers. The remaining 8.8 million pounds came from direct channels.

Some 12% of the total collected volume was refurbished and resold, but that’s a figure that does not include what its certified recyclers did. What these figures mean is that of a total volume of nearly 39 million pounds, the company managed to place 12% into the secondary market.

Given that Sony is moving away from PCs and focusing on high-end TV technology, it is expected that its recycling activity for both PCs will shrink substantially.

Sony’s recycling is relatively decent when compared to some larger competitors in the US market. HP for instance, which is among top-tier in the US IT space, it recycled some 50 million pounds in 2011 in the North America region. Subtracting Canada from the number and the US figure gets closer to Sony’s.

While these companies seem to generate relatively growing volumes of electronics at the end of their lifespan each year, there is a great deal of volumes of electronics that remain uncollected. Even when compared to professional e-Cyclers activity, OEMs have somewhat limited direct contribution based on the basic data we observed. For example, while Sony collected some 39 million pounds, that is close to the volume mid-tier ITAD companies like Regency Technologies or Redemtech collected by in 2009. In the case of HP, its 2011 volume of 50 million pounds is equivalent to ECS Refining or a Round2 Inc back in 2009. This means that large manufacturers that are responsible for massive amounts of hardware should be able to do much better than a mid-tier ITAD company.

Yet, for a company like Sony, which needs to reduce its cost and move all its business units to profitability, a reduction in recycling program cost will help toward that goal.

For professional recyclers, Sony’s deemphasizing of PC and TV hardware does not pose an immediate threat per se. The company after all holds a low-single digit share of the PC market, and its share of the US TV market dropped to below 3%, under intense pressure from Korean manufacturers. But what recyclers should be concerned is that while some of the lost Sony business will eventually go to competitors, Sony’s refocus on content and mobile hint on trends that will inevitably affect recyclers in the long run. Emerging devices from tablets and smartphones, to wearables with content ubiquitously available are expected to alter the new equipment market and eventually the secondary and recycling markets.

.[/membersonly]